People can understand simple things with ease, so “simple” is a great place to start when explaining new concepts to others. Focusing on simple concepts gives people a foundation where they can make connections and later build on those new ideas. But even seemingly simple ideas, like so many things, often are much more complex than they first appear.

What is “simple”? For most of us, reading is simple. You probably weren’t even thinking about reading as you read the previous paragraph. That is because reading has become second nature to you — but it didn’t start that way. I remember the labor of learning to read in kindergarten and first grade. Letters were 52 incredibly complex shapes that had sounds associated with them, with two different versions of each, further complicated by how a capital “I" and a lowercase “l” appear to be the same character. This is only to say that what we take for granted today was a struggle a few years ago. (Okay, maybe more than a few years for some of us.) The point is that “simple” differs based on what you know at the time.

We all learned to read by establishing a firm foundation as a starting point. Shapes are the foundations for letters, sounds are associated with letters, and when shapes are put together they create words. My teacher did not pressure us to start with complex ideas, like non-phonetic words — she would introduce those later on. The learning process requires that the initial foundation be one that can be built upon. Therefore, selecting the appropriate foundation is critical.

Now let’s apply this concept to retirement planning. What is a good foundation? What lays the groundwork for shapes to become sounds, sounds to become words, and words to become reading? Where should someone start?

But first, let’s ask a bigger question: How is the industry doing as a whole?

At a recent board meeting, an outside evaluator said we had “a lot of potential.” It was a backhanded compliment. The financial services industry has plenty of evidence of our “potential,” but we could be doing better. Many Americans are not on the path for a properly funded retirement, and many of those who have access to a retirement plan are not moving in the right direction. I believe that much of the industry is missing the building blocks of retirement readiness.

I believe most advisors have the best intentions: they want their clients to be prepared for retirement, and they want to engage them to move forward. Advisors are passionate about their job, but they take for granted their ability to “read” in the retirement planning world while their clients are still looking at letter shapes they do not understand.

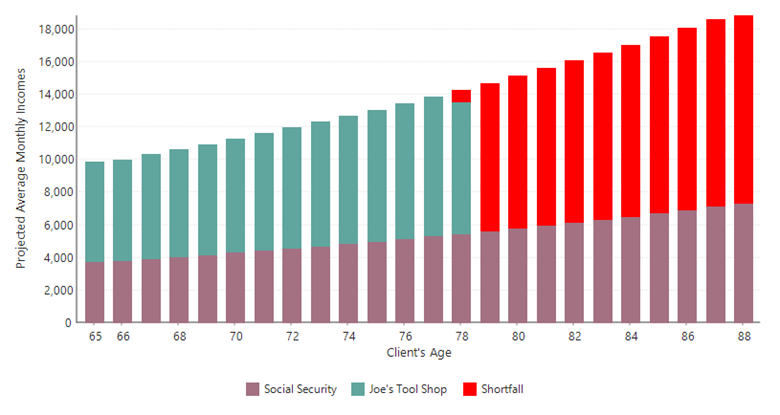

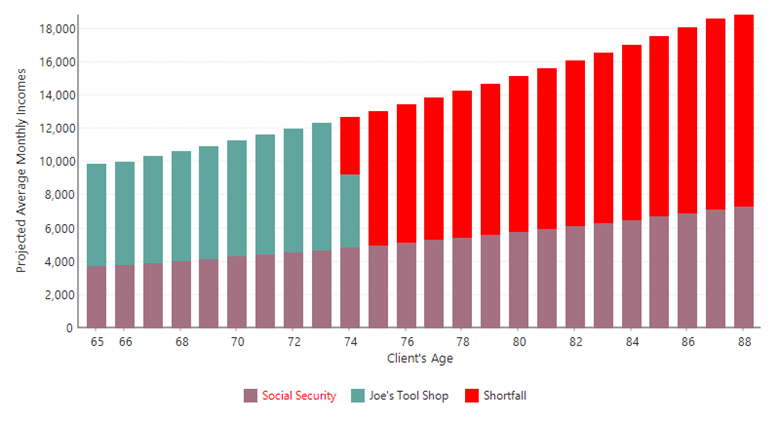

The most effective tool I have consistently seen advisors use to overcome this challenge is the integrated retirement needs analysis chart (shown below). This is a basic building block that nearly everyone can understand — and it helps everything else make sense in the retirement planning world. For example, I could easily use this chart to illustrate or explain the impacts of rates of return, additional savings, and changes in retirement age, inflation, and so much more. This chart provides the context for explaining the essential elements of retirement planning.

Let me provide an example. Suppose an advisor wanted to talk about how fees impact retirement savings. We all know this is a critical aspect of retirement planning. The advisor could talk about it abstractly (stressing how lower fees are important), show some numbers (an excellent step forward, but potentially confusing or intimidating for many people), or quickly modify the data to emphasize how increased fees result in a different outcome. The last tactic provides meaningful, visual information on what fees do for retirement in a way that everyone understands.

I know several advisors who leverage this chart to heighten the clients’ (or plan participants’) engagement. When this chart is displayed, they ask their clients how they want to address the shortfall. Then they sit quietly and let the clients think about the problem for themselves, often for the first time. Too often, clients rely on advisors to think and never become truly engaged in the retirement planning solution. One advisor shared with me that her client called her up two weeks later to ask if she could make a change! (The client is thinking about it that long!). This simple building block for connecting clients to their retirement planning process can build engagement and grow AUM.

The key takeaway here is that advisors need to keep retirement planning simple. Think through which building blocks you can use to engage your audience in a meaningful way, and what foundation you can build upon that provides meaning and context for everything else.

Edward Dressel is President, RetireReady Solutions.

Opinions expressed are those of the author, and do not necessarily reflect the views of the NTSA or its members.

- Log in to post comments